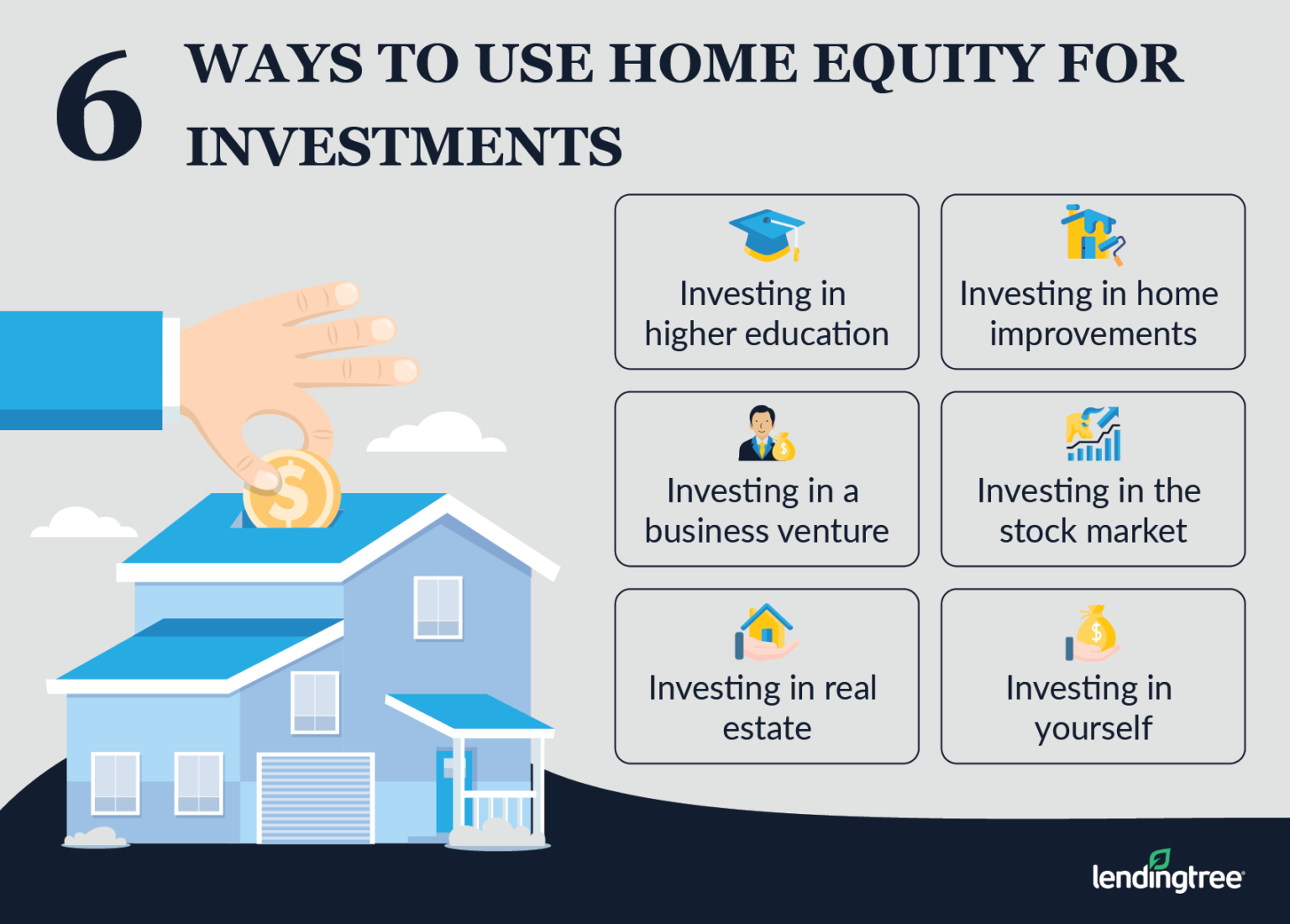

The bottom line into Consolidating Obligations Into the Mortgage

Because Borrowing Counsellors, our company is will questioned, might you consolidate financial obligation towards home loan repayments? Thinking is the fact from inside the doing so, you’ll slow down the total appeal you only pay into the your individual expenses (because the mortgage rates will likely be all the way down) and you will provide probably a lot of money monthly.

Sometimes, combining financial obligation for the home financing will cost you. However, first, why don’t we consider just how it works.

Consolidating Personal debt Towards Mortgage loans: The way it operates

Very house possess collateral in them. Equity is the difference between the value of your house and you can what exactly is owed with the financial.

For example, say you reside really worth $200K therefore only owe $125K towards the home loan. It means you have got $75K value of equity. Better yet, since you continue to reduce your mortgage, equity will continue to increase (a spike in worth of together with grows they, when you find yourself a decline inside property value, however, decrease they). That $75K was a fantastic amount of transform, proper? Therefore in cases like this, you could contemplate using it to blow off several of the high-focus balances of the deciding to consolidate the debt into a mortgage that you refinanced.

Merging obligations to your a home loan inside Canada mode breaking your current mortgage contract and you can going high-appeal bills (particularly credit debt, payday loans, or any other low-mortgage balance) for the an alternative home loan set within a special (hopefully) lower interest rate. This will be either considering the shorthand identity regarding debt consolidating home loan or consolidation mortgage because of the particular (regardless of if a loan provider would probably balk within term integration financial.)

After you’ve done this, your mortgage financial obligation increase from the number of non-financial financial obligation you folded involved with it, plus a couple thousand bucks alot more into the price of breaking the dated home loan and a potential Canada Mortgage and Homes Organization (CMHC) premium into increased home loan balance. The latest upside would be the fact, in principle, the interest you have to pay on the non-mortgage personal debt often disappear.

A few When Consolidating Personal debt into the Mortgages

Figuring out if or not a debt consolidation home loan will benefit you inside brand new much time-work on relies on of many circumstances. All the financial is different, so there are merely so many variables to add a black and you may light answer-it’s all grey!

Such, many people will have to thought whether they may even qualify to own a different sort of financial to own merging loans with respect to the brand new laws and regulations to mortgages today. You might also need to adopt this new financial price you could get on brand new revival.

Could it possibly be almost than your existing price? When it is more, really does the fresh reduction of interest which you yourself can shell out in your non-financial expenses exceed the increase in the mortgage interest possible avoid upwards paying? Before you combine your debt on the a home loan, talking about all of the questions you really need to believe!

There is also the price of the newest penalty to have cracking your current home loan, the potential brand new CMHC superior, including one legal costs inside. Sometimes, your property may prefer to getting examined, and that will charge a fee some money also.

These are things you’ll need to think of to genuinely determine if merging loans into your financial is the better solutions to you. If you want to know very well what the brand new effect off deciding to combine loans to your home loan repayments will appear to be for you particularly, you might want to think talking-to the financial otherwise borrowing from the bank connection.

Combining Obligations Towards the an initial-Day americash loans Branchville Financial

What if you’re not a recently available homeowner, however they are considering to order property? You happen to be capable combine the debt into the home financing when buying another family. Becoming eligible, lenders will appear at your mortgage-to-value (LTV) proportion to search for the chance your twist since the a debtor. LTV is the size of the loan compared to the value of the property you want to get.